Residual Commission: How Recurring Revenue Comp Works

Residual commission pays reps on renewals, not just the initial close. Learn how it works, typical rates, common structures, and when it makes sense for SaaS.

Most commission plans pay once. A rep closes a deal, earns commission, and moves on to the next one. That model works fine when revenue is transactional — a product ships, the relationship ends, done.

It breaks down once your revenue is subscription-based.

If a customer signs a $60,000 ARR contract, stays for four years, and then churns — was that actually a $240,000 relationship or a $60,000 deal? The way you answer that question shapes whether residual commission belongs in your comp plan.

What is residual commission?

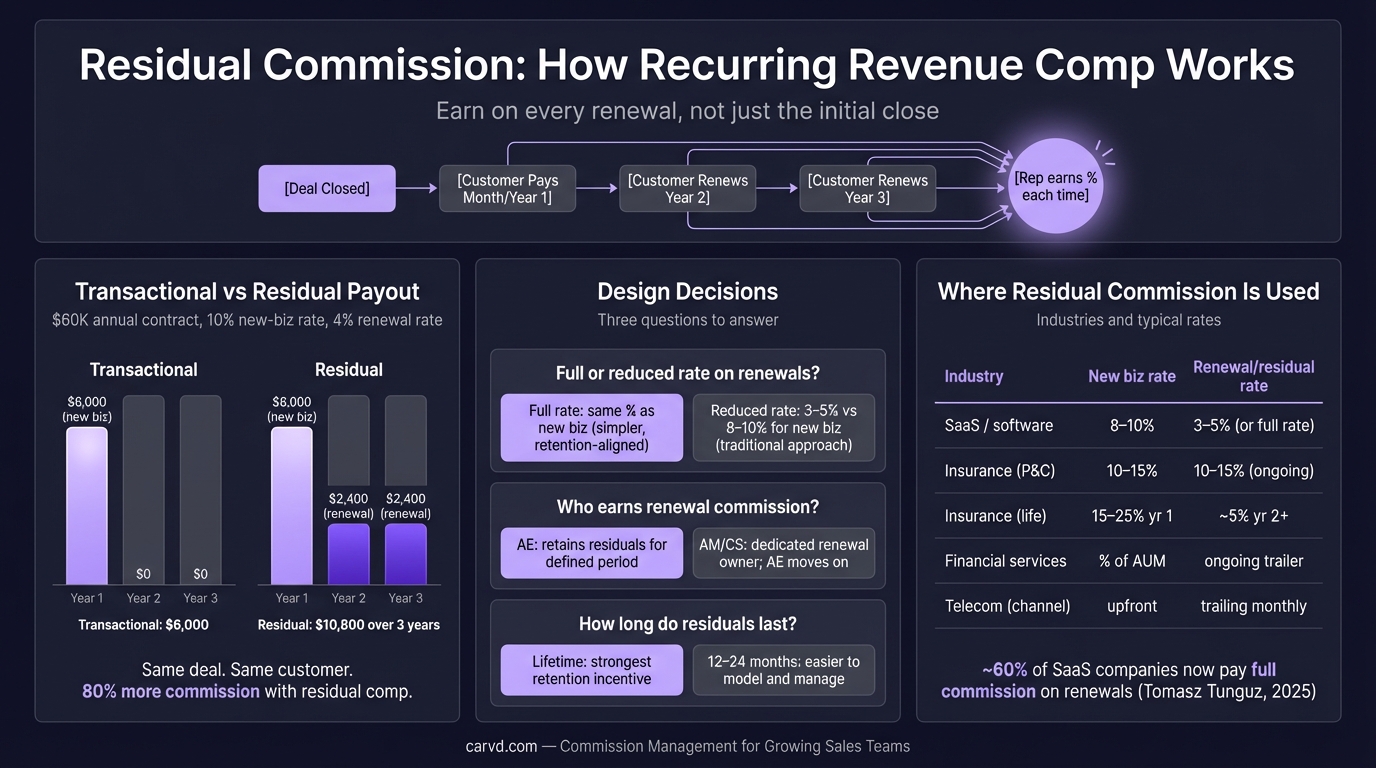

Residual commission is commission paid on an ongoing basis as long as a customer continues to pay. Rather than a single payout at close, the rep earns a percentage of the recurring revenue each period the customer renews or continues their subscription.

The term originated in industries where trailing income is structurally built into the product — insurance agents have earned residual commissions on policy renewals for decades, and financial advisors earn trailing fees on assets under management. In SaaS and subscription software, the same concept applies: reps who close recurring contracts can earn a percentage of that revenue for as long as the customer stays.

The distinction from a standard commission is timing. Standard commissions are front-loaded — paid at close, often based on first-year contract value. Residual commissions spread over the life of the customer relationship.

Where residual commission shows up

Insurance: Agents typically earn a reduced commission on policy renewals — often 2–5% versus 10–20% for new policy acquisition. Renewals can make up a significant portion of a senior agent's income.

Financial services: Registered investment advisors and wealth managers often earn trailing commissions or ongoing advisory fees as a percentage of assets under management.

SaaS and subscription software: Renewal commissions are the subscription equivalent. A rep might earn 10% on new ACV at close, then 3% on renewal ACV each year the customer stays.

Managed services and telecom: Monthly recurring revenue (MRR) commissions are common — reps earn a percentage of the monthly contract value for each month the customer remains active.

How residual commission works in SaaS

In SaaS, residual commission and renewal commission refer to the same thing. The question is whether your company pays it at all — and if so, at what rate.

According to the 2016 Pacific Crest SaaS Survey, 60% of SaaS startups paid some form of renewal commission, typically around 3% of ACV — compared to 8% for new business. The other 40% paid nothing on renewals.

The 2018 Viola Ventures SaaS Sales Compensation Annual Survey found a similar split: 50% of companies paid no commission on renewals, 22% paid at a reduced rate, and about 6% paid the same rate as new ACV.

That means in a given cohort of SaaS companies, roughly half pay nothing when a customer renews. Whether that's the right call depends on your organizational structure and comp philosophy.

Common residual commission structures

Reduced rate on renewal ACV

The most common approach among companies that pay renewal commissions. The rep earns a percentage of the renewal contract value — typically 2–5% versus 8–15% for new business.

Example: An AE closes a $48,000 ARR deal and earns 10% = $4,800 at close. If the company pays a 3% renewal commission, the AE earns $1,440 each year the customer renews.

Over a three-year relationship: $4,800 + $1,440 + $1,440 = $7,680 total, compared to $4,800 on a new-business-only plan.

No renewal commission — expansion only

Pay nothing on flat renewals, but pay new-business rates on upsells and expansions. The logic: maintaining a contract doesn't create new value; growing it does. This structure is increasingly common as CSMs take over renewal ownership.

Quota credit modifier

Rather than a separate commission rate, some companies (per Alexander Group's 2024 XaaS compensation analysis) apply a credit multiplier — for example, renewal ACV counts at 0.5x toward quota while new logo ACV counts at 1.5x. The rep earns the same commission rate, but the effective payout per renewal dollar is lower because fewer quota credits are awarded.

Milestone-based with clawback

Pay most of the commission upfront, but claw back a portion if the customer churns within 90–180 days. Mark Roberge documented HubSpot's use of this approach in The Sales Acceleration Formula — splitting commission payments at first payment, six months, and twelve months, which increased average customer prepayment commitment from 2.5 months to 7 months.

The ownership question

Before designing a residual commission structure, answer who owns renewals.

According to ChurnZero's 2024 Customer Success Leadership Study of 1,000+ CS leaders, sales team ownership of renewals dropped from 15% of companies in 2023 to 8% in 2024. Dedicated renewal teams own renewals at 15% of companies; CS teams are absorbing more of this responsibility.

If your CSMs own renewal outcomes — meaning they're the ones preventing churn, handling escalations, and driving QBRs — paying AEs a residual commission on that revenue creates a misalignment. AEs get paid for work CSMs are doing.

If your AEs own the full customer relationship (common in smaller teams or enterprise account management roles), some ongoing commission makes sense as a signal that their job doesn't end at signature.

There's no universal answer. The right structure follows accountability.

The case for residual commission

It incentivizes reps to close good-fit customers. A rep on a new-business-only commission plan has no financial stake in whether the customer actually succeeds. Residual commission changes that calculus — the rep earns more from a customer who stays than from one who churns after 90 days.

HubSpot found more than a 10x difference in churn rates across individual AEs — one rep at 35% account churn, another at 7%. Commission structures that reward retention over pure volume can close that gap.

It aligns incentives with your revenue model. A SaaS company's value is its recurring revenue. Paying commissions only on new logos sends the message that renewals don't matter. That's a disconnect when 80%+ of revenue comes from existing customers at most mature SaaS companies.

It rewards reps who build real relationships. An enterprise AE who invested 14 months building a relationship with an account might reasonably expect some ongoing recognition beyond a one-time close.

The case against residual commission

It creates harvest behavior. Reps with large books of renewal income are less motivated to hunt for new logos. Senior reps spend time farming existing accounts instead of developing new pipeline. This is a real problem in high-tenure sales organizations.

It adds comp complexity. Every active customer becomes a calculation. When does the residual period end — year 2? Year 5? What happens if the account is reassigned? Multi-year contracts, expansions, and account transfers all create edge cases that require clear policy.

It may not align with your org structure. If CSMs own renewals, AEs earning residuals creates noise — payouts to people who aren't doing the work.

Calculating residual commission

The formula is straightforward:

Renewal ACV × Renewal commission rate = Commission per period

For monthly residuals: (MRR × Rate) / 12 if you're paying annually, or MRR × Rate for monthly payouts.

The complexity isn't the math — it's tracking which customers are live, what their renewal value is, which rep gets credit, and when the residual period expires. At five reps, a commission spreadsheet template can manage it. At 25 reps with three plan types and a mix of new logos and renewals, the spreadsheet becomes the source of disputes.

Tools like Carvd track both new-business and renewal commission calculations automatically via CSV deal import or CRM sync, showing each rep exactly which customers are generating residual income and how the amounts were derived.

When residual commission makes sense

Consider adding renewal commissions to your plan when:

- Renewal responsibility genuinely sits with the sales team (not CSMs)

- Customer churn is a material concern and you want reps financially invested in retention

- You're in an industry like insurance, financial services, or managed services where trailing income is standard

- Your AEs are expected to manage accounts post-close and renewal outcomes are within their control

Skip residual commission (or limit it to expansion only) when:

- CSMs own renewals and you don't want conflicting incentives

- You want reps exclusively focused on new pipeline

- The comp complexity isn't worth the overhead at your current team size

Either way, the decision should be explicit — not a default. Most commission disputes around renewals come from ambiguity in the plan document, not disagreements about intent. A clear dispute resolution workflow helps resolve the inevitable edge cases without eroding trust.

For a broader look at how residual commission fits within the full range of plan structures, see the sales commission structure guide. Related structures worth comparing: tiered commission, which accelerates payouts above quota, and draw against commission, which addresses income floors rather than tails.

Last updated: March 21, 2026