Commission Clawbacks: When to Use Them (And When Not To)

Commission clawbacks recover paid commissions when deals cancel or customers churn. Learn how to structure them, set the right window, and avoid the morale trap.

A commission clawback is one of those plan mechanics that creates more conflict than almost any other decision in sales comp — not because it's inherently unfair, but because it's usually introduced after a problem rather than designed in from the start.

Done well, a clawback policy protects the company from paying for revenue that doesn't stick, and creates a useful incentive for reps to close the right customers. Done poorly, it functions as a punishment applied retroactively to deals reps had no reason to doubt.

Here's how to think about whether you need one, how to structure it, and where most companies get it wrong.

What a commission clawback is

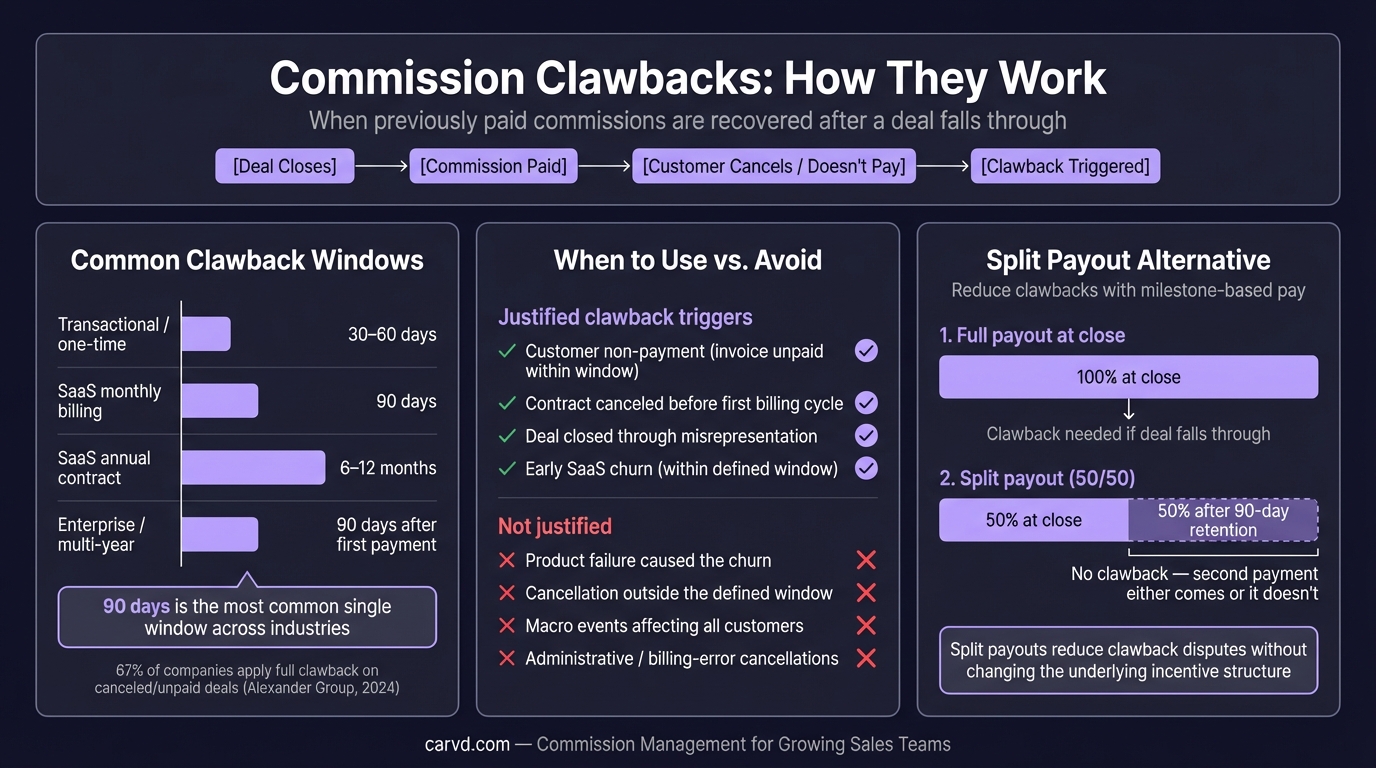

A commission clawback is the recovery of previously paid commission when a deal falls through after close. The most common triggers:

- A customer cancels the contract before a defined period (often 90 days)

- A customer fails to pay their invoice

- A deal was closed using unapproved discounts or misrepresentation

- A SaaS customer churns within the first quarter after activation

Commission clawback definition: A commission clawback is the recovery of previously paid commission when a deal falls through — typically due to customer non-payment, contract cancellation, or early churn within a defined window after close.

This is distinct from a draw against commission, where an advance is recovered from future commissions. A clawback reaches back into already-paid earnings. That's why it's more sensitive — and why the policy design matters so much.

Why companies use clawbacks

The core problem a clawback solves: a rep earns their commission at close, but the company doesn't get paid (or keeps the revenue) until later. If those two events never align, the company absorbs the cost of a commission for a deal that didn't hold.

This is particularly common in:

SaaS and subscription businesses. Monthly or annual recurring revenue is only valuable if the customer stays. A rep who closes 50 bad-fit accounts and churns them all by month 3 has technically hit their quota while costing the company money.

Businesses with net-payment terms. If customers are invoiced Net-30 or Net-60, a commission paid on close may be paid before the customer actually pays. If the invoice goes unpaid, the company has paid commission on a deal that produced no cash.

High-discount environments. Without some downside for bad deals, reps can be incentivized to close at any margin, any terms, to any customer. A clawback on churned accounts is one mechanism to counteract that.

According to the Alexander Group's 2024 Sales Compensation Trends Survey, 67% of companies apply a full clawback on non-payment and canceled orders. Fewer than 5% allow reps to keep commissions on deals that are canceled or go unpaid — meaning most sales organizations treat some form of clawback as standard.

When clawbacks are justified

Customer non-payment. If your commission is contingent on the customer paying their invoice, a clawback on unpaid deals is straightforward. The commission wasn't earned until cash was collected; the clawback simply enforces that condition.

Early cancellations. For SaaS especially, a 90-day cancellation window is common. If a customer cancels before their first invoice or within the first billing cycle, it's reasonable to treat the deal as unclosed. A clawback in this window is defensible.

Deal fraud or misrepresentation. If a rep closed a deal through false commitments to the customer — promises that led to an inevitable cancellation — a clawback is appropriate regardless of timing.

Significant early churn. Some SaaS companies extend clawbacks to 6–12 months to account for customers who made it through onboarding but churned early. This is more contentious, but defensible if reps have real influence over who they sell to.

When clawbacks are not justified

Churn driven by product failure. If a customer churns because the product didn't deliver on what was sold in the marketing materials, engineering didn't ship a promised feature, or the customer support experience was poor, clawing back the rep's commission creates resentment without improving the outcome. The rep sold what was available to sell.

Deals outside the clawback window. A customer who churns in month 13 of a 12-month clawback window cancels within the subscription period, but not within the window. Applying discretionary clawbacks outside the defined period destroys trust faster than any single bad deal.

Macro churn events. If a downturn, COVID-style disruption, or industry shock causes customers to cancel en masse, a company-wide wave of clawbacks punishes the entire team for conditions no rep could have predicted or prevented. This is a time to waive the policy, not enforce it mechanically.

Administrative cancellations. Duplicate contracts, billing errors, or internal company restructuring that causes a contract to be reissued rather than genuinely canceled are not churn events.

The practical rule: if the rep couldn't have changed the outcome with better selling, the clawback serves no behavioral purpose and only creates a morale problem.

How to set the clawback period

The clawback window should be tied to when you'll know if a deal is genuinely going to hold.

| Business type | Typical clawback window | Rationale |

|---|---|---|

| Transactional / one-time purchase | 30–60 days | Returns and cancellations are handled quickly |

| SaaS monthly billing | 90 days | First billing cycle, first renewal |

| SaaS annual contract | 6–12 months | First renewal, full onboarding period |

| Enterprise / multi-year | 90 days after first payment | Payment is often the clearest signal |

Ninety days is the most common single window across industries. For SaaS companies where customer health only becomes clear over a longer period, extending to 6 months is reasonable — but the longer the window, the more contested specific clawbacks become. Reps who closed a deal eight months ago often have limited recollection of why, which makes disputes harder to resolve.

The split payout alternative

One approach that reduces clawback frequency: pay commissions in two installments rather than all at close.

Example: 50% of commission paid at close, 50% paid after 90 days of verified customer retention.

This isn't technically a clawback — it simply defers half the payment until the deal has proven itself. Reps typically find this easier to accept than a full clawback policy because there's nothing to "take back." The second payment either comes or it doesn't.

The operational tradeoff is that you need to track deal status at the 90-day mark for every closed deal, every quarter. That's manageable with software; it's painful in a spreadsheet. A commission spreadsheet template can handle the initial tracking, though you'll outgrow it quickly as deal volume scales.

Legal considerations

Clawback policies need to be in writing before the first commission is paid. Retroactive clawback policies — introduced after deals have closed — are legally risky and practically unenforceable.

California is the most restrictive state. Under California Labor Code Section 221, employers generally cannot recoup wages already paid. A chargeback is only enforceable against advance commissions (money paid before the commission was legally "earned" under the plan terms). Once a commission is fully earned under the written plan, clawing it back is heavily restricted. If you have California-based reps, structure your plan so that commissions aren't "earned" until customer payment — not at close.

In most other US states, clawbacks are enforceable if the commission was not yet fully earned at the time of the clawback — for example, if the plan document specifies that customer payment is a condition of earning the commission. The key is having that condition in writing before the deal closes.

Plan documentation requirements: Most states require commission agreements to specify when commissions are earned, how they're calculated, and any conditions for recovery. California explicitly requires this in writing (Labor Code Section 2751). Even outside California, written commission agreements are essential for enforcing any clawback.

If your plan includes clawbacks, the plan document should answer:

- What events trigger the clawback

- How long after close the clawback period runs

- How the clawback amount is calculated (full commission, prorated, net of taxes already paid?)

- How disputes are handled

The rep trust problem

Clawbacks are one of the fastest ways to damage trust between sales ops and the sales team — not because reps object to the concept, but because they're often applied inconsistently.

Common failure modes:

Clawbacks applied after the policy was changed. If you introduce or extend a clawback policy mid-year, reps who closed deals under the old policy will feel retroactively punished.

Clawbacks without explanation. If a rep receives a deduction on their paycheck without a clear breakdown of which deal, which trigger, and how the amount was calculated, they'll dispute it — and that dispute will cost sales ops hours to resolve. A dispute resolution workflow that shows the original deal, the triggering event, and the clawback math prevents most of these escalations.

Clawbacks that exceed the rep's current commission balance. A clawback that creates a negative balance (the rep "owes" money) is particularly contentious. In most states, deducting this from future wages is legally complicated and practically destructive to retention.

If clawbacks are triggering more than 15-20% of closed deals, the problem is likely deal qualification, not individual rep behavior. The right response is to address the qualification process, not tighten the clawback window.

What to include in a clawback policy

A clawback policy that reps will accept — and that holds up if disputed — should include:

-

Trigger definitions. Specifically what events cause a clawback (non-payment after X days, cancellation within X days, churn within X months). Use dates and thresholds, not qualitative descriptions.

-

Clawback period. The window during which clawbacks can be applied. After this period, commissions are final.

-

Calculation method. Full commission, prorated commission, or net of taxes already withheld? This matters especially if you're clawing back commissions from a prior tax period.

-

Exceptions. What events explicitly don't trigger clawbacks (product failure, company-wide force majeure events, administrative cancellations).

-

Dispute process. How a rep can contest a clawback, who reviews disputes, and the timeline for resolution.

-

Recovery method. Deduction from next paycheck, deduction from future commissions, or invoice to the rep. The method matters legally in some states.

Tracking clawbacks accurately

The operational challenge with clawbacks is that they're calculated after the period closes — sometimes months after the deal appeared in your commission run.

In a spreadsheet, this typically means:

- Manually identifying which deals in prior periods were canceled or unpaid

- Looking up what commission was paid on those deals

- Calculating the clawback amount

- Applying it as an adjustment in the current period

Each step is error-prone, and reps often dispute the math. The most common disputes come from:

- Inconsistent application of the clawback window (did the cancellation fall inside or outside the period?)

- Disagreement about whether the triggering event was a real cancellation or an administrative one

- Calculation errors in the original commission payment that affect the clawback amount

Tools like Carvd maintain an audit trail of every commission paid, by deal and by period. When a clawback is triggered, you can pull the original payout record, apply the clawback calculation, and show the rep exactly what's being recovered and why. That transparency doesn't eliminate disputes, but it significantly reduces them.

Clawbacks vs. other ways to align incentive timing

Clawbacks aren't the only way to tie commissions to deal quality. A few alternatives:

Milestone-based payouts. Pay commissions in installments tied to deal milestones: close, first payment, first renewal. Reps earn commissions on the timeline the revenue actually arrives, without a retroactive clawback mechanism.

Customer health bonuses. Instead of punishing churn with clawbacks, reward retention with a bonus at 12 months. This flips the framing from punishment to reward — and is often more effective at changing behavior.

Adjusted commission rates by deal type. Lower commission rates on higher-risk deal types (short-term contracts, heavy discounts, non-standard terms) changes the incentive at the point of sale rather than after. The commission plan builder lets you model these risk-adjusted rate structures before rolling them out to the team.

None of these fully replaces a clawback policy for non-payment situations, but they can reduce how often clawbacks are needed.

For more on how clawback policies fit into broader compensation plan design, see the guide to sales commission structures. For the mechanics of advance commission payments — which are often recovered in a similar way — see draw against commission explained.

Related reading

- Sales commission structure types — how clawbacks fit into flat, tiered, and draw-against plans

- Draw against commission explained — advance payments and how they're recovered

- Straight commission: is it right for your team? — the structure where clawback policies carry the most weight

- Base salary plus commission: finding the right split — how guaranteed base changes the clawback calculation

Last updated: March 21, 2026