Draw Against Commission: How It Works (With Examples)

Learn how draw against commission works, the difference between recoverable and non-recoverable draws, and how to structure one for new sales hires.

A new enterprise AE closes their first deal in month four. Their quota is $600,000 annual ACV. Until that first close, their commission is zero.

That's the problem a draw against commission solves. It provides a guaranteed payment floor during the period between hiring and earning, so reps can afford to ramp without financial pressure that pushes them toward bad deals.

Here's how draws work, when to use them, and how to avoid the mistakes that create payroll and legal problems.

What is a draw against commission?

A draw against commission is an advance payment to a sales rep that is offset against commissions they earn in the same or future periods. The rep receives a predictable monthly payment during ramp — and that payment is later reconciled against earned commissions.

Draws are most common in:

- Enterprise and complex sales — long average sales cycles mean reps can't close immediately

- Pharmaceuticals and medical devices — relationship-driven selling with extended decision timelines

- Financial services — new advisors and brokers building a book of business

- Technology hardware — high-value equipment with long procurement cycles

- Media and advertising sales — reps building agency relationships before first revenue

The unifying factor: roles where a new hire can't generate meaningful commission income in their first 60 to 90 days, regardless of effort.

Recoverable vs. non-recoverable draws

There are two types, and the distinction matters for both payroll math and rep behavior.

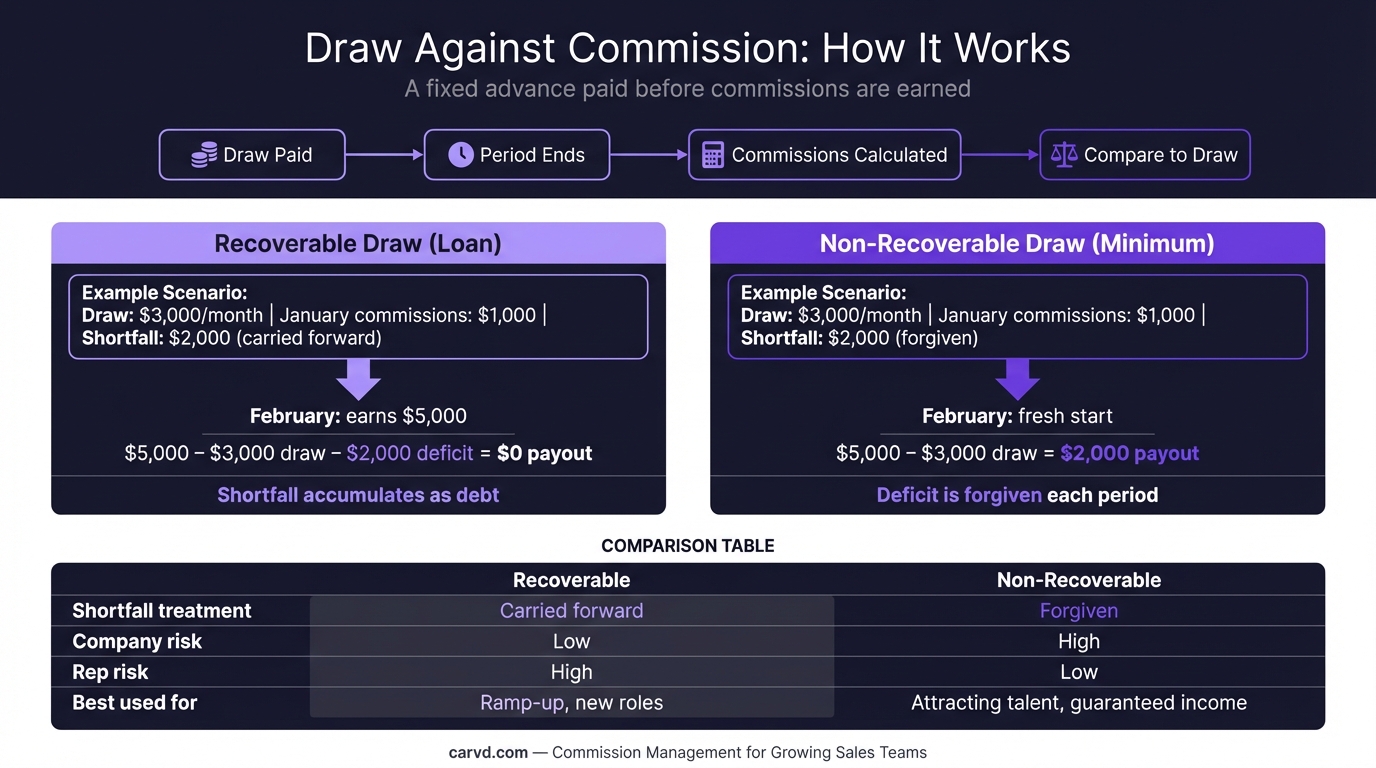

Recoverable draw

A recoverable draw functions as a loan. The company advances cash each period; earned commissions are applied against that advance. If commissions fall short, the shortfall carries forward as a balance the rep repays from future earnings.

Example: A new field sales rep has a $3,000/month recoverable draw. In month one, they earn $900 in commissions.

- Rep receives $3,000 total (draw covers the gap)

- Deficit: $2,100 carried forward to month two

In month two, they earn $4,500 in commissions.

- $2,100 repays the month-one deficit

- $900 is applied to the current month's draw

- Remaining $600 is paid out as commission above the draw

Recoverable draws protect the company's cash outlay. They're most common for internal transfers onto a new territory or product — situations where a rep doesn't need heavy training, just time to rebuild pipeline.

Non-recoverable draw

A non-recoverable draw is a guaranteed income floor. If commissions fall short, the rep keeps the draw amount and owes nothing. If commissions exceed the draw, the rep receives their commissions in full — the draw isn't subtracted again.

Example: Same rep, same $3,000/month draw, but non-recoverable. Month one: $900 earned.

- Rep receives $3,000

- No balance carried forward

- Company absorbs the $2,100 shortfall as a cost

Month two: $4,500 earned.

- Rep receives $4,500 (commissions exceeded draw; no offset)

- Company pays $4,500 with no recovery of prior shortfalls

Non-recoverable draws are standard for new external hires. The reasoning is practical: you hired someone who can't sell yet because they're in training, not because they're underperforming. Penalizing them for a deficit they couldn't avoid is both unfair and a retention risk.

According to Sales Comp Academy, most companies offer non-recoverable draws for external hires and recoverable draws for internal transfers, where training overhead is lower and ramp expectations are higher.

How long should a draw last?

Most draws run 3 to 6 months. A rule of thumb from Xactly: ramp period = average sales cycle length + 90 days.

A SaaS AE with a 45-day average deal cycle would have a ramp period of roughly 4.5 months. A pharma rep with a 6-month sales cycle would need closer to 9 months.

The Bridge Group's 2017 SaaS AE benchmark found that 41% of companies report average ramp times of 5 months or longer for account executives — making a 3-month draw potentially insufficient for complex-sale environments.

You can model different ramp durations and their impact on OTE using the OTE calculator before finalizing the draw period. A progressive taper structure handles this well:

| Ramp period | Draw amount |

|---|---|

| Months 1–3 | 100% of target variable |

| Months 4–6 | 75% of target variable |

| Months 7–9 | 50% of target variable |

| Month 10+ | Standard commission only |

The taper signals to reps that the draw is transitional — not a permanent floor — while giving them meaningful support through the full ramp window.

How much should the draw be?

According to Sales Comp Academy, draw amounts typically range from 75% to 100% of a rep's target variable compensation for the draw period.

For an AE with $150,000 OTE split 50/50 base/variable, the variable component is $75,000 annually, or $6,250/month. A full draw at 100% of target variable would be $6,250/month. At 75%, it's $4,688/month.

Setting the draw too low undermines its purpose — a rep who can't cover rent won't be focused on ramping. Setting it too high with no taper removes urgency and can create dependency on the draw rather than building toward commission income. Model draw scenarios in a Stackrows financial template.

Draw against commission vs. guaranteed salary

A draw is not the same as a guaranteed salary, though they can look identical on a pay stub during ramp.

The practical difference: a guaranteed salary has no offset against commission. A draw is always reconciled — either per period (recoverable) or as a floor (non-recoverable). Once earned commissions exceed the draw amount, the rep earns above the draw, not in addition to it.

This matters when designing comp plans. A rep on a non-recoverable draw of $4,000/month who earns $6,000 in commissions receives $6,000 — not $10,000. The draw is a floor, not a bonus.

Legal risks employers need to know

Post-termination recovery is legally impermissible in the US. In Stein v. hhgregg (2017), the Sixth Circuit Court of Appeals ruled that requiring employees to repay draw advances after termination violates the FLSA's minimum wage requirements. Wages must be paid "free and clear" — and even an unenforced repayment policy creates liability through psychological pressure on former employees.

Pre-termination recovery from current commission payments is generally permissible, but varies by state.

California has additional requirements. All commission plans — including draws — must be documented in a written agreement specifying how commissions are computed and paid. A signed copy must be given to every employee. Failure to document creates exposure even if the draw arrangement itself is legal.

Rest break compliance. In California, a recoverable draw does not satisfy the employer's obligation to compensate reps for rest breaks. Even if the draw is large enough to cover minimum wage for all hours worked, rest periods must be separately compensated.

Draws that create significant balances — particularly in the first 90 days — are worth reviewing with employment counsel, especially if you operate in California, New York, or states with aggressive wage recovery protections.

The case against draws

Draws solve an income timing problem, but they create administration complexity. Every draw period requires:

- Reconciling draws against earned commissions per rep

- Tracking running balances for recoverable draws

- Managing the taper schedule and transition to standard commission

- Handling edge cases (rep leaves with a balance, territory change mid-draw, deal credited in wrong period)

For teams under 15 reps, this is manageable in a spreadsheet if plans are simple. For teams with multiple plan types and ramp stages, the reconciliation burden compounds quickly. Carvd's comp plan builder lets you configure draw rules alongside standard commission plans so reconciliation happens automatically each cycle.

Some companies sidestep the draw entirely by offering a higher base salary for the first 6 months, then transitioning to a lower base with full commission. It achieves similar income stability with simpler payroll mechanics.

Others use a salary-plus-commission structure where the guaranteed base is sufficient for income during ramp — making a draw unnecessary. See base salary plus commission for how to design the right split.

When to use a draw

A draw makes sense when:

- Reps are hired into roles with sales cycles longer than 60 days

- You're hiring externally into a territory that needs to be built from scratch

- Competitive hiring conditions require income certainty to attract experienced reps

- You want to reduce first-year voluntary attrition among new hires

It's probably not worth the complexity when:

- Your average deal cycle is under 45 days (reps should be generating commission income within their first month)

- You have fewer than 5 reps and can manage onboarding individually

- You're hiring experienced reps who know the industry and have transferable pipeline

Tracking draws alongside commissions

Draw reconciliation — matching advances to earned commissions across multiple periods — is where manual tracking tends to break down. A rep with a 6-month recoverable draw and variable deal flow will have different deficit balances every period, which need to carry forward accurately.

Carvd tracks draw advances and earned commissions together, so reconciliation happens automatically as part of each commission run. Reps see their current draw balance and what they'd need to earn to generate a payout above the draw — which matters for rep trust as much as it matters for ops accuracy.

The short version

A draw against commission is a period-based income advance, reconciled against earned commissions, used primarily during sales rep ramp periods. Non-recoverable draws are standard for new external hires; recoverable draws suit internal transfers. Set the draw at 75–100% of target variable, taper it over 3–9 months depending on cycle length, and document the terms in writing before the rep's start date.

The legal exposure from improper recovery — particularly post-termination — makes the written documentation non-optional in any state.

For a side-by-side comparison of how Carvd handles draws versus other platforms, see how Carvd compares to Core Commissions.

Related reading: Sales Commission Structures: Types, Examples & How to Choose · Commission Clawbacks: When to Use Them · Base Salary Plus Commission: Finding the Right Split · Tiered Commission Structure: How to Build One That Scales

Last updated: March 21, 2026