Commission Accounting: Revenue Recognition Under ASC 606

ASC 606 requires most sales commissions to be capitalized and amortized, not expensed immediately. Here's what qualifies, how amortization works, and the mistakes that trigger audit risk.

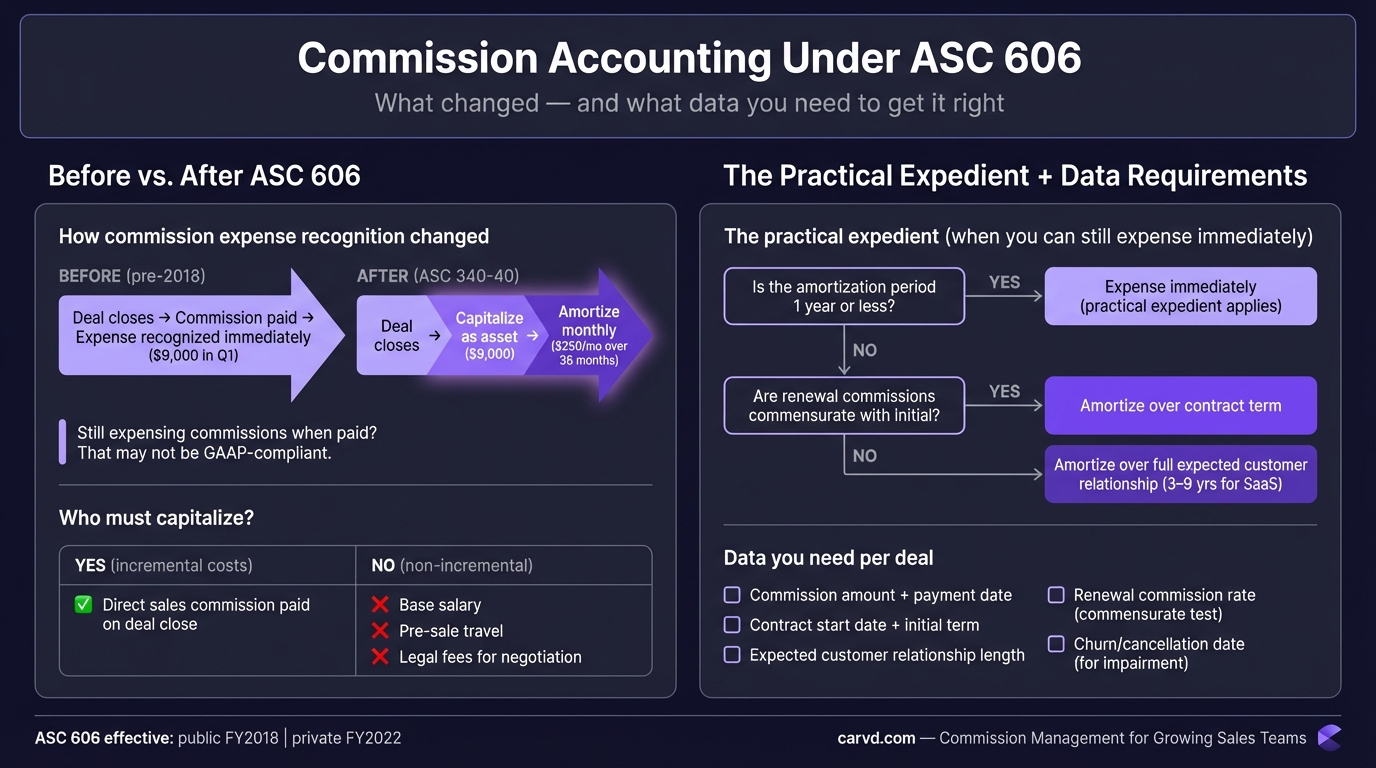

Under ASC 606, how you recognize sales commission expense on your income statement changed fundamentally. For most SaaS and subscription businesses, commissions paid to close customer contracts must be capitalized as an asset and amortized over the expected customer lifetime — not expensed the month they're paid.

That's a significant departure from the pre-2018 norm, when most companies simply deducted commissions as an expense when paid. Getting it wrong creates audit risk, misrepresents profitability, and in public companies, has drawn SEC comment letters.

What ASC 606 changed for commission accounting

The old approach was simple: pay the commission, debit expense, credit cash. The new standard introduced ASC 340-40, the contract costs subtopic that accompanies ASC 606. It requires that incremental costs of obtaining a contract be recognized as an asset — provided the entity expects to recover those costs through future revenue.

For most sales organizations, this means capitalized commissions show up on the balance sheet as a deferred commission asset, and that asset gets amortized over time in line with when the related services are delivered.

Public companies were required to adopt for fiscal years beginning after December 15, 2017. Private companies had until fiscal years beginning after December 15, 2021 (extended by COVID-related FASB deferrals). If you're a private company that adopted recently, your prior comparison periods may not reflect the new treatment.

Which commissions must be capitalized

The test is a but-for test: would this commission have been paid if this specific contract had not been obtained?

Costs that typically qualify for capitalization:

- Sales commissions paid directly upon deal close

- Bonuses explicitly tied to obtaining a specific contract

- Payroll taxes on commissions (since they're incremental to the same payment)

- Manager override commissions on deals closed by their team (still incremental to each contract)

Costs that do NOT qualify (expensed immediately):

- Base salaries — paid regardless of whether any deal closes

- General performance bonuses based on overall metrics, not specific contracts

- Travel, entertainment, and proposal costs

- Marketing and advertising expenses

- Bonuses contingent on future employee service periods (considered compensation for future periods)

The nuance matters. If a sales manager earns an override on every deal their team closes, that override still qualifies as incremental to each specific contract — even though it flows to someone who didn't directly sell the deal.

The practical expedient: when you can skip capitalization

ASC 340-40-25-4 provides a practical expedient: if the amortization period of the capitalized asset would be one year or less, you may expense the commission immediately rather than capitalizing it.

For businesses selling short-duration contracts — annual or shorter — this can eliminate the accounting complexity entirely.

Two things to watch:

Renewals extend the clock. The one-year test isn't just the initial contract term. You must consider anticipated renewals. A nine-month contract that routinely auto-renews for another 9 months probably doesn't qualify for the expedient — the expected amortization period is 18+ months.

It's an all-or-nothing election. You can't apply the expedient contract-by-contract. It must be applied consistently to all contracts with similar characteristics. If you elect it, disclose it in your financial statements.

How amortization works

Once you've determined a commission must be capitalized, you need to amortize it on a systematic basis consistent with when you transfer goods or services to the customer.

In practice, that means the amortization period is the expected customer lifetime — contract term plus reasonably anticipated renewals, supported by historical data on renewal rates and customer churn.

The commensurate renewal rule is the critical decision point for SaaS companies.

If your renewal commissions are commensurate with initial commissions — proportional to the contract value they generate — you can amortize just over the initial contract term. But if initial commissions are significantly higher than renewal commissions (which is typical in SaaS, where a rep earns 10-15% on new business and 3-5% on renewals), the initial commission is considered compensation for landing the full customer relationship, not just the first-year contract. You have to amortize over the full expected customer life.

For a SaaS company with a 3-year average customer lifetime and front-loaded commissions, that means spreading the commission expense over 36 months rather than 12 — a material difference in reported profitability in early quarters. Carvd's commission calculator maintains deal-level records that map directly to amortization schedules, so finance teams can trace each capitalized asset back to its originating contract.

When commissions must be written off early

Capitalized commission assets are subject to impairment testing. If a customer terminates their contract before the end of the amortization period, the remaining unamortized balance must be written off immediately.

This matters for companies with high early-churn customers: if you capitalize commissions assuming a 36-month customer life but a meaningful percentage cancel in month 8, you're carrying overstated assets until the impairment is recognized. Regular impairment testing — at least annually, and when triggering events occur — is required. Tools like Everstage and CaptivateIQ offer enterprise-grade ASC 606 modules, but many mid-market teams find a simpler solution covers their compliance needs without the implementation overhead.

Draws against commission

Draws complicate the accounting further. The treatment depends on whether the draw is recoverable or non-recoverable.

Recoverable draws (the rep must repay them from future commissions) are advances — a receivable on your balance sheet, not a commission expense. They're not contract costs under ASC 606 and aren't capitalized. When future commissions are earned and offset against the draw balance, that's when the expense hits.

Non-recoverable draws (guaranteed minimums the rep keeps regardless of what they close) are compensation expense. They don't meet the incremental cost test — the company would pay them whether or not any specific contract was obtained. They're expensed immediately and not capitalized.

For a detailed breakdown of draw mechanics, see draw against commission.

Common mistakes

Treating all commissions as immediately expensed. The pre-ASC 606 default. Still common at smaller private companies that adopted recently or haven't been through an audit that scrutinizes it.

Using only the initial contract term for the amortization period. For SaaS companies with front-loaded commissions, this understates the amortization period and overstates early profitability.

Applying the practical expedient to contracts with anticipated renewals. The expedient is only available when the true amortization period — including renewals — is one year or less.

Forgetting impairment on early terminations. Commission assets don't automatically write off when a customer churns. You need a process to identify terminations and trigger write-offs.

Not reconciling commission accounting to commission payroll. Commission payroll runs and accounting entries need to reconcile. If your commission tracking lives in a spreadsheet separate from your GL, discrepancies accumulate and create audit exposure — importing deals via CSV deal import ensures the same data feeds both your commission calculations and your accounting records. Commission reporting and commission errors both trace common gaps here.

What this means for commission operations

Accurate commission accounting under ASC 606 requires knowing, deal by deal, exactly what was paid and when — not just a lump monthly total. That means your commission tracking needs to maintain deal-level records that can be matched to accounting periods, amortization schedules, and termination events.

For teams still tracking in spreadsheets, the ASC 606 treatment adds a layer of complexity that often exceeds what manual processes can handle reliably. If you're not yet ready for software, Stackrows finance templates can help organize deal-level records for the interim. A commission spreadsheet can calculate what to pay; it can't easily maintain the ongoing amortization schedule, handle impairment, or reconcile to your GL without significant manual work.

Tools like Carvd calculate commissions at the deal level with full audit trails, which gives your finance team the deal-by-deal records needed for accurate capitalization and amortization schedules.

Quick reference: ASC 606 commission accounting

| Scenario | Accounting treatment |

|---|---|

| Commission on deal close (standard SaaS) | Capitalize, amortize over expected customer life |

| Commission on deal close (contract term ≤1 yr, no renewal expected) | Practical expedient — expense immediately |

| Commission on deal close (contract term ≤1 yr, renewals expected) | Likely must capitalize — test for >1 yr amortization period |

| Base salary of sales rep | Expense immediately — not incremental |

| Recoverable draw (advance against future commissions) | Balance sheet receivable, not commission expense |

| Non-recoverable draw (guaranteed minimum) | Compensation expense — expense immediately |

| Early contract termination | Write off remaining unamortized commission asset |

For more on the operational side of commission tracking — including how commission formulas translate into payroll-ready numbers — see the commission-ops posts in this series.

Last updated: March 22, 2026