ASC 606 and Sales Commissions: What Finance Teams Need to Know

ASC 606 requires most sales commissions to be capitalized under ASC 340-40. Here's the journal entry treatment, disclosure requirements, and what auditors look for.

ASC 606 changed how most sales organizations recognize commission expense. Before 2018, the standard approach was simple: pay the commission, book the expense. Under ASC 340-40 — the contract costs subtopic created alongside ASC 606 — that approach is now non-compliant for most businesses with subscription or multi-year contracts.

This post covers the mechanics that matter most to finance teams: the incremental cost test, the journal entry treatment, disclosure requirements, and what auditors focus on when they review commission capitalization.

For background on the core concepts — which commissions qualify, how the practical expedient works, and amortization period decisions — see commission accounting under ASC 606.

The incremental cost test

ASC 340-40-25-2 defines what must be capitalized: costs that are incremental to obtaining a specific contract — that is, costs that would not have been incurred if the contract had not been obtained.

For most sales commissions, this is a but-for test. Would the commission have been paid if this specific contract had not been signed? If yes, it's incremental and must be capitalized (subject to the recovery test). If no — if it would have been paid regardless — it's expensed immediately.

Two elements must both be satisfied:

- Incremental cost test: The cost is only incurred because this contract was obtained

- Recovery test: The entity expects to recover those costs through future revenue from the contract

Base salaries fail the incremental test — they're paid whether or not any deal closes. Discretionary bonuses based on overall team performance typically fail it too. A sales commission paid directly upon signing a specific contract passes it.

The nuance: manager overrides and payroll taxes on commissions also pass the incremental test, because they arise directly from the same contract-specific commission that triggers them. Many finance teams expense these by default — that's a misapplication of the standard.

Journal entry treatment

Here are the standard journal entries for commission capitalization under ASC 340-40:

At contract signing — capitalize the commission:

| Account | DR | CR |

|---|---|---|

| Capitalized Contract Costs (Asset) | $12,000 | |

| Commissions Payable | $12,000 |

When commission is paid:

| Account | DR | CR |

|---|---|---|

| Commissions Payable | $12,000 | |

| Cash | $12,000 |

Monthly amortization (example: 36-month expected customer life, straight-line):

| Account | DR | CR |

|---|---|---|

| Amortization Expense — Contract Costs | $333 | |

| Capitalized Contract Costs | $333 |

Amortization runs through SG&A. Some companies run commissions through payroll first and use a contra-expense entry to reclassify to the asset, then amortize back into SG&A over the benefit period. Either approach is acceptable as long as the ending balance sheet and income statement positions are identical.

Balance sheet classification: The portion of the asset expected to amortize within 12 months is current; the remainder is non-current. If you have a $36,000 capitalized commission asset with 30 months remaining, $12,000 is current and $24,000 is non-current.

Early termination — write off the remaining asset:

| Account | DR | CR |

|---|---|---|

| Impairment Loss — Contract Costs | $18,000 | |

| Capitalized Contract Costs | $18,000 |

Impairment is recognized immediately when a contract terminates before the end of the amortization period. The remaining unamortized balance cannot be left on the balance sheet.

Disclosure requirements

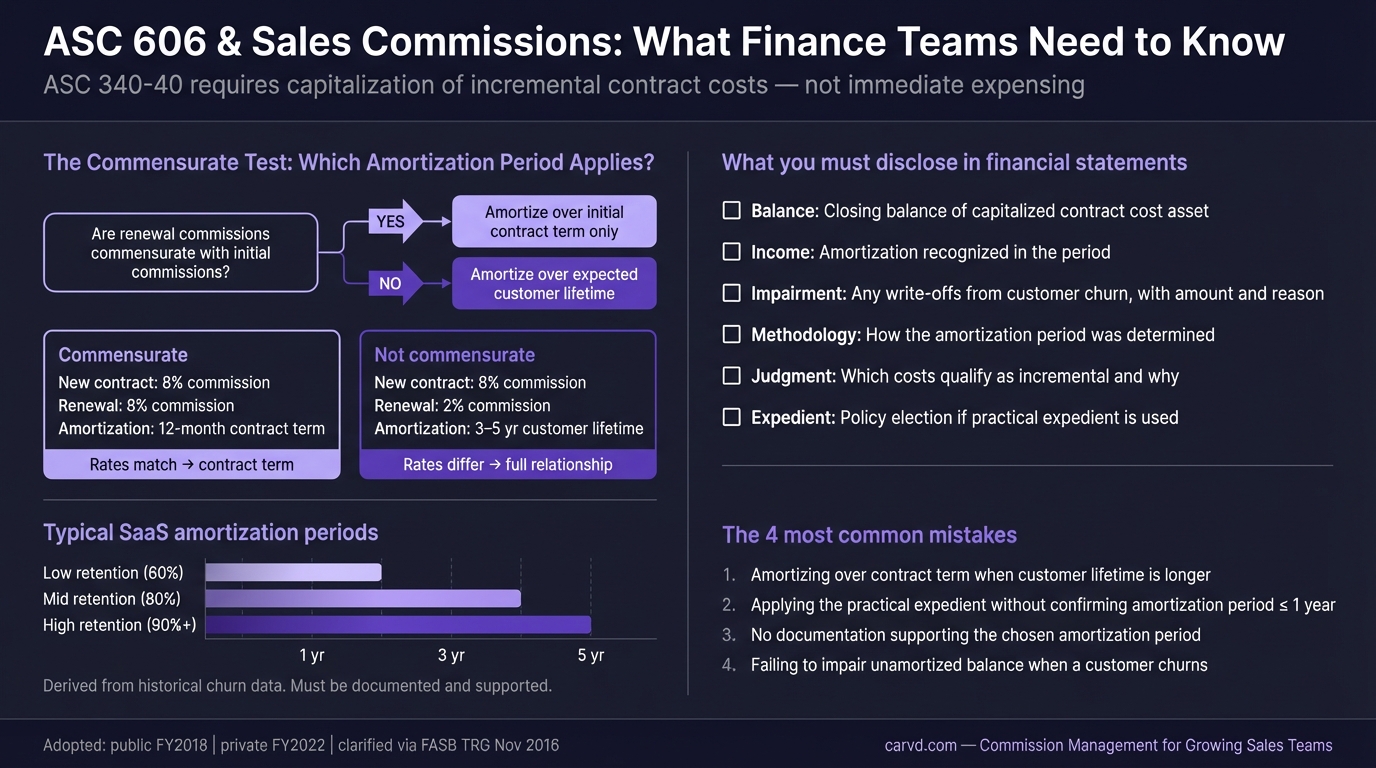

ASC 340-40-50-1 through 50-3 sets out what must be disclosed in the financial statements. Most finance teams underdisclose here, which is the most common finding in SEC comment letters on this topic.

Required disclosures:

1. Qualitative description of judgments: Which costs qualify as incremental and why. Simply stating "sales commissions are capitalized" is not sufficient — auditors want to see how the incremental test was applied and what cost categories were evaluated and excluded.

2. Amortization method and period: The systematic basis used, how the benefit period was determined, and whether anticipated renewals were considered. This is the most common SEC comment area (see below).

3. Closing balances: The ending balance of capitalized contract cost assets for the period, broken out by type if material (e.g., separate line items for initial commissions, renewal commissions, payroll taxes).

4. Amortization expense for the period: Total amortization recognized in each reporting period.

5. Impairment losses: Any impairment charges recognized during the period.

6. Practical expedient election: If you elect to expense incremental costs immediately for contracts where the amortization period would be one year or less, that policy election must be disclosed. It must also be applied consistently — you can't apply it contract-by-contract.

Private companies benefit from some relief on ASC 606-10-50 disclosures (e.g., disaggregation of remaining performance obligations), but the ASC 340-40 contract cost disclosures above apply to all entities.

What auditors and the SEC look for

According to Deloitte's March 2019 Heads Up analysis of SEC staff comment letters in the first year of public-company adoption, nearly 10% of all ASC 606 SEC staff comments related specifically to contract costs under ASC 340-40. Two issues dominated:

Issue 1 — Amortization period doesn't account for renewals

The most common comment: companies selected an amortization period equal to the initial contract term without considering anticipated renewals. The SEC's position is that if the company routinely renews contracts, the benefit period extends through renewals, and the amortization period must reflect that.

A nine-month contract that auto-renews for another nine months doesn't qualify for the practical expedient — and shouldn't be amortized over nine months even if you can't use the expedient. The expected amortization period is 18+ months.

Issue 2 — The commensurate test applied incorrectly

If renewal commissions are commensurate with initial commissions — proportional to the contract value they generate — amortization can be limited to the initial contract term. But if initial commissions are significantly higher than renewal commissions (as is typical in SaaS, where a rep earns 10% on new business and 3% on renewals), the initial commission is compensation for landing the full customer relationship. It must be amortized over the full expected customer life.

Companies frequently assert commensurateness without the data to support it. Auditors are now asking for deal-level data showing commission rates at initial signing versus renewal to validate the claim. A commission calculator that tracks rates at the deal level produces exactly the data auditors request — initial vs. renewal rates, per contract, with timestamps.

System requirements for compliance

Accurate ASC 340-40 accounting requires deal-level commission records, not just period totals. Your commission data needs to support:

- Contract-level traceability: Each capitalized asset traces to a specific contract, with the signing date, initial commission amount, and expected amortization period

- Amortization schedules: Calculated and maintained for each capitalized commission, updated when contract terms change or when renewals extend the benefit period

- Termination events: A process to identify customer churn events and trigger impairment write-offs on the associated commission assets

- Renewal rate data: Historical renewal rates to support the amortization period assumptions you're disclosing

- Reconciliation to payroll: The commission amounts capitalized need to reconcile to what was actually paid, which requires deal-level data from the same system that runs commission payroll — the payroll export bridges this gap by sending the same deal-level totals to both your GL and your payroll provider

Teams tracking commissions in spreadsheets hit two specific walls with ASC 340-40: the spreadsheet calculates what to pay, but it doesn't maintain amortization schedules or link payment records to contract termination events. A Stackrows financial template can help organize the initial calculation, though you'll still need a dedicated tracking layer for ongoing amortization. Monthly reconciliation of the capitalized asset balance requires a manual tracking layer that most spreadsheet setups don't have.

Tools like Carvd calculate commissions at the deal level with full audit trails, giving finance teams the deal-by-deal records they need for capitalization, ongoing amortization schedules, and reconciliation to payroll.

Adoption timeline and transition

Public companies were required to adopt ASC 606 and ASC 340-40 for fiscal years beginning after December 15, 2017. Private companies' deadline was extended multiple times — the final required adoption date, set by ASU 2020-05, was annual periods beginning after December 15, 2021.

Enterprise tools like Xactly or CaptivateIQ handle ASC 606 reporting, but many mid-market teams find them overbuilt for their needs. If your company is a recent private-company adopter, two things to verify:

Prior-period comparatives: Depending on the transition method chosen (full retrospective or modified retrospective), prior-period financial statements may or may not have been restated. If you used modified retrospective, the cumulative adjustment as of the adoption date went through retained earnings — not prior-period comparatives. Make sure your financial statement users understand this.

Accumulated deferred commission balances: If your company has multi-year customer contracts and had never capitalized commissions before adoption, the transition creates a catch-up on existing contracts. The deferred commission asset recognized at adoption date represents commissions paid on contracts that were still open at that date, reduced by amortization you would have recognized if ASC 340-40 had always applied. This is a material balance for SaaS companies with long average customer lifetimes.

For more on the operational side — how commission plan structures affect the amounts being capitalized, and how commission reporting supports the data your finance team needs — see the related posts in the commission operations series.

Last updated: March 22, 2026